On March 26 and March 27, 2026, the S&P 500 Index dropped 1.74% and 1.67%, respectively. This two-day decline totaling 3.38% is an event that happens, on average, only once or twice a year. Over the course of March, the S&P 500 Index was down 7.2% as of March 27. Based on the timing of these drawdowns, the rise in oil prices from the Iran conflict appears to be a key driver.

The interdependence of asset markets and household income seems to have been forgotten amid the AI hype over the last few years. That may be because investors have gotten used to sailing on calm seas. While President Trump has caused market volatility via disruptive, short-lived initiatives, these have neither targeted nor largely affected the consumer.

Tariffs have come the closest, but policy reversals, flexible and innovative supply chains, and the U.S. Supreme Court have combined to produce a muted net effect on Main Street – at least until the administration’s escalation of tensions with Iran. This opened a direct line to household spending via the spike in oil prices.

Oil recently reached just over $110 a barrel. Social media and news organizations have howled over the spike. However, based on history, oil prices have reached significantly higher levels in the past. Peak oil prices were reached in July 2008. Adjusted for inflation, that peak is approximately $215 a barrel.

How damaging could elevated oil prices be for the economy? History and an analysis of household income suggest that the recent oil-driven stock market declines may reflect concerns that oil prices could remain elevated.

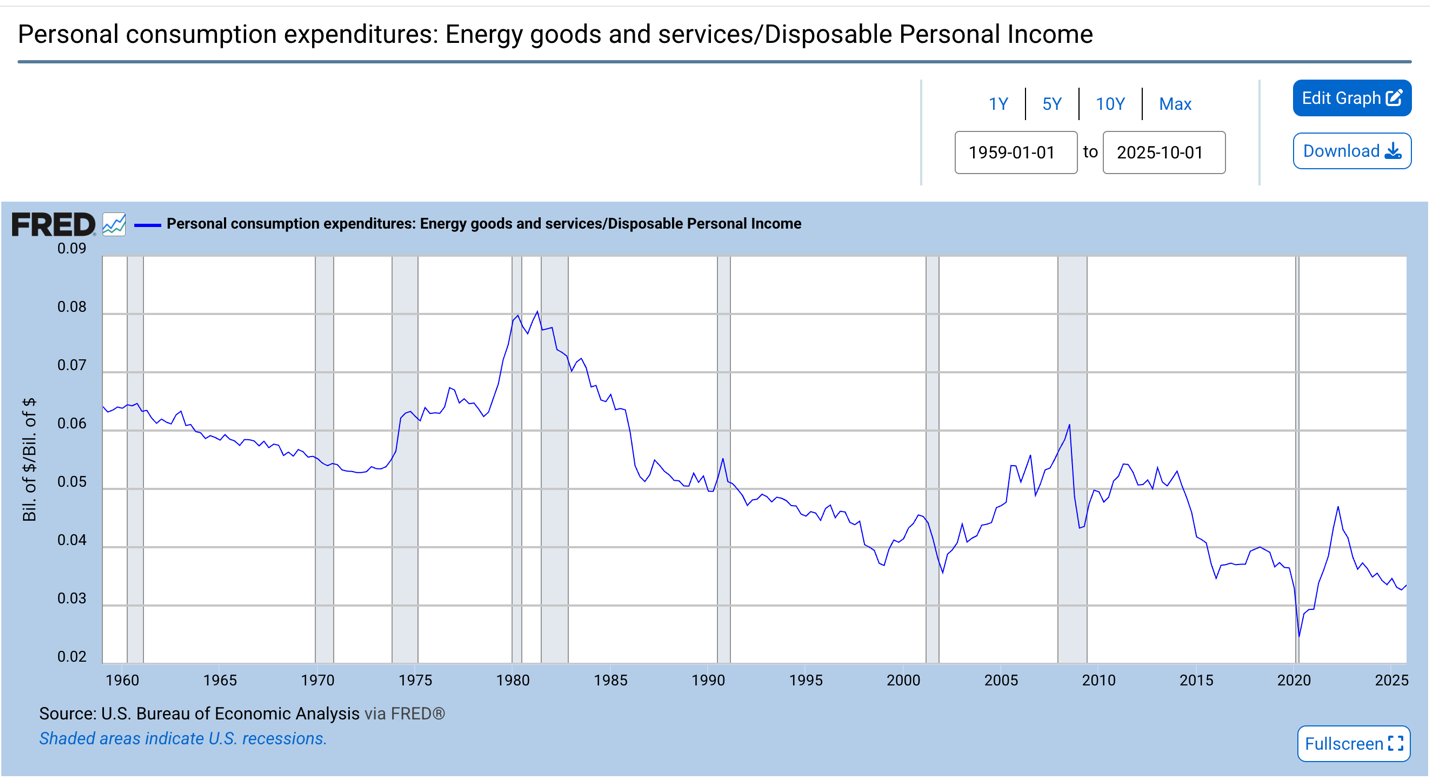

The following chart plots the percentage of income that American households spent on energy consumption from January 1959 through September 2025.

Source: U.S. Bureau of Economic Analysis, Federal Reserve Bank of St. Louis.

A few observations jump out. First, households typically spend approximately five percent of their income on energy. Second, since 2015, oil expenditures have trended to historic lows. This is driven heavily by a sustained period of moderate-to-low oil prices. Third, spikes in oil prices have at times been associated with recessions. The oil price spike in 2022, following the Russian invasion of Ukraine, resulted in significant market volatility and a small drop in the market. The volatility occurred despite the fact that the spike in oil prices only modestly increased energy expenditures from historically low levels. One can imagine the effect on income expenditure if oil prices were to double.

For middle- and lower-income families, a doubling of oil prices could be the equivalent of a significant tax on already stretched consumers. And there is a double whammy with a spike in oil prices: Since oil is an input to many goods, oil price spikes tend to come with inflation. A potential jump in inflation comes with higher interest rates and could represent a significant headwind to consumer spending.

Will calmer heads prevail and shield markets from potentially damaging policies? It probably isn’t so simple this time; it will not be easy to back out of the Iran war. The Strait of Hormuz likely needs to be opened for oil prices to ease, which may require significant time and military resources, including ground troops and a complete defeat of the hardline Iranian regime – otherwise, the Strait will continually be vulnerable.

If oil prices stay elevated for a sustained period of time, markets could experience broader impacts. Even the AI juggernaut that has been driving the stock market higher has been (literally) fueled through lower energy prices keeping the cost of training AI models muted.

Investors be aware: Markets and consumers still appear quite vulnerable to a shock in oil prices. With a war driving the disruption in these oil markets, President Trump may have stumbled into something he cannot bully into submission – the supply side of the economy.

For active managers, the primary risk factor in the market may be shifting from exposure to AI to exposure to oil prices. These risks are different in nature, particularly along their timeline. The returns to AI exposure have unfolded and will continue to unfold over years, whereas oil price shocks have historically been resolved on a shorter time horizon.

With oil prices having nearly doubled since the start of the year, energy now accounts for a growing share of household spending, rising from around 3% to nearly 6%. According to U.S. Census Bureau Data, for the average U.S. family earning about $85,000 a year, this translates roughly to $2,500 more spent on energy. These shifts could have ripple effects across consumer behavior as households decide where to trim spending to offset higher energy costs.

If the market is focused on a shorter-term risk factor, we might expect more volatility as AI sentiment on the long run profitability of this breakthrough technology remains slower moving. However, that volatility may look less idiosyncratic in the cross-section than that which occurred from the second half of last year.

For a global asset management firm like Intech, the current environment underscores the importance of adaptive risk models (those capable of accounting for both near-term shocks and long-duration innovation cycles) helping inform conversations about how to navigate rapidly-evolving sources of market risk.

About Intech

Intech is a global quantitative asset manager that applies advanced mathematics and systematic portfolio rebalancing to harness a reliable source of excess returns and a key to risk control – stock price volatility. Intech applies its investment approach across five investment platforms which differ by risk-return objective: relative or absolute. Intech also integrates fundamental-based information to identify stocks with favorable underlying characteristics, complementing its volatility-based models that target stocks with attractive trading profit potential due to their volatility characteristics. These strategies only differ by the client’s desired benchmark and risk budget and include enhanced equity, active equity, defensive equity, extension equity, and absolute return investment solutions within the U.S., global, and non-U.S. regions.