Introduction

Global equity markets delivered an exceptionally strong second quarter with nearly every major benchmark posting double-digit gains. Beneath those headline returns, however, market leadership became increasingly concentrated as semiconductor and AI-related companies accounted for a disproportionate share of performance.

At the same time, the macro backdrop improved meaningfully. Geopolitical tensions surrounding the Strait of Hormuz eased late in the quarter which reduced inflation concerns and improved expectations for monetary policy. While market leadership remained narrow, broader participation began to emerge beneath the surface.

This paper examines the three themes that defined Q2 and their implications for equity markets in the third quarter.

Theme 1: Markets Discounted a Geopolitical Resolution

Takeaway: Markets looked beyond the temporary energy shock and increasingly priced in an improving macroeconomic environment.

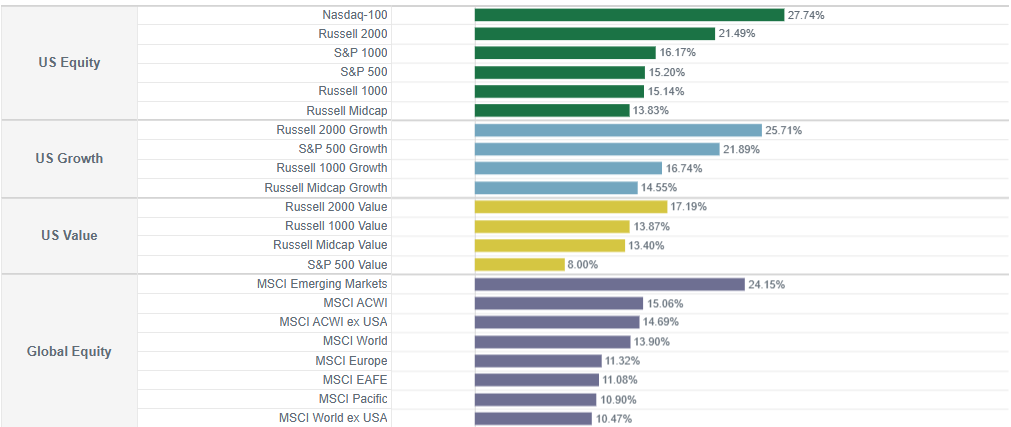

Figure 1:

Equity Markets Performance – Q2 2026

Despite one of the most significant geopolitical events in years, global equity markets finished the quarter with impressive gains. The Nasdaq-100 and Russell 2000 Indices each returned more than 20%. Emerging Markets delivered comparable strength and nearly every major developed market posted double-digit returns. Markets increasingly looked beyond the temporary energy shock and began discounting an improving macroeconomic environment.

For much of the quarter, Iran and the Strait of Hormuz remained the dominant macro risk. Higher oil prices pushed inflation expectations higher, reduced expectations for Federal Reserve rate cuts, and contributed to one of the most divided FOMC votes in decades as policymakers balanced inflation risks against slowing growth.

Conditions changed materially late in June 2026. The U.S.-Iran agreement reopened shipping through the Strait, eased restrictions on Iranian oil exports, and significantly reduced concerns over global energy supply. Oil prices declined sharply from their May highs, financial conditions improved, and Energy became the weakest-performing sector as markets anticipated normalization well before the agreement was finalized.

Investor sentiment also remained remarkably resilient. The successful SpaceX IPO highlighted continued demand for long-duration growth assets despite elevated valuations and geopolitical uncertainty. It appears that investor risk appetite remained strong heading into the second half of the year.

What to Watch

The geopolitical backdrop has improved materially, but the pace of normalization remains important. Continued declines in energy prices would reinforce the disinflation trend and strengthen the case for Federal Reserve easing later this year. Conversely, renewed disruptions to shipping or oil production could quickly reverse those gains and reintroduce inflationary pressures.

Oil prices, inflation expectations, and Fed communication could remain the key indicators to monitor during Q3.

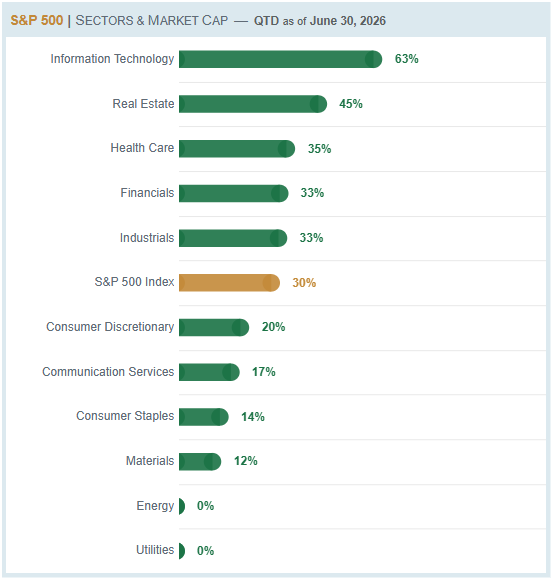

Theme 2: AI Leadership Became Increasingly Concentrated

Takeaway: Semiconductor stocks drove returns across sectors, styles, and regions, leaving market leadership increasingly concentrated.

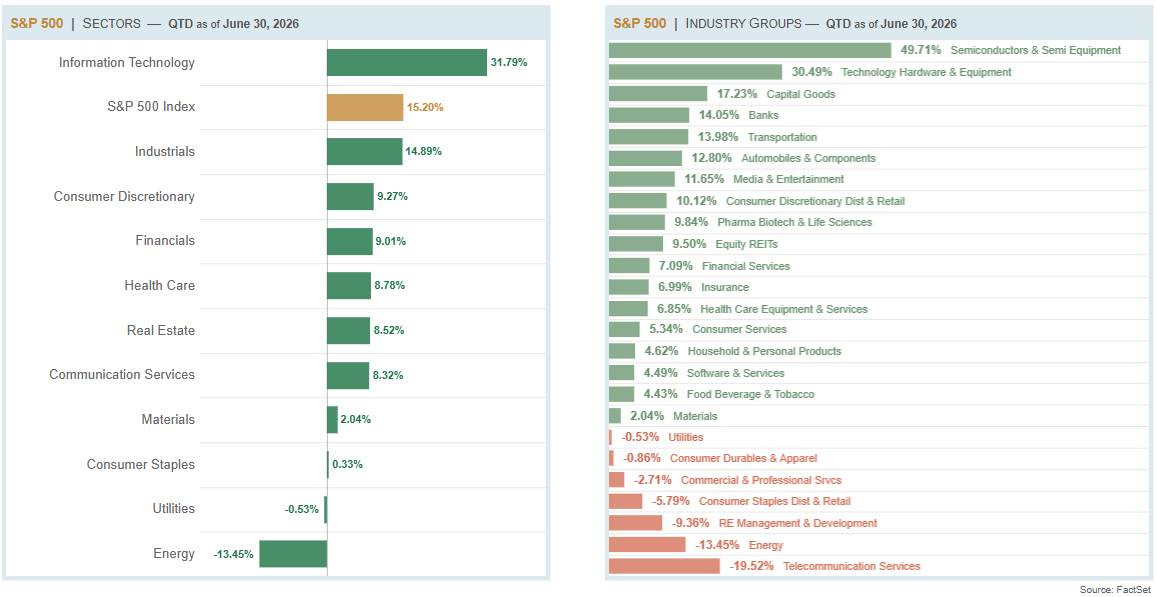

Figure 2:

S&P 500 Index Sector and Industry Group Performance – Q2 2026

Although global equity markets rallied broadly, leadership became increasingly concentrated across regions. Information technology was the only sector to outperform across the major U.S. and global equity benchmarks, while only three of the 25 GICS industry groups outperformed the broader market in both the S&P 500 and the MSCI World Indexes. Semiconductor & Semiconductor Equipment generated the strongest gains by a wide margin, whereas Energy and Communication Services ranked among the weakest sectors.

The concentration extended well beyond sectors. Value, growth, and momentum strategies all benefited from exposure to many of the same semiconductor companies. Intel and Micron, for example, represented meaningful positions in several factor portfolios, allowing one industry group to drive returns across multiple investment styles simultaneously. As a result, multi-factor diversification provided less protection than investors typically expect.

Participation within the largest companies also remained narrow. Only a relatively small share of mega-cap stocks outperformed despite lifting capitalization-weighted indices higher. The quarter’s gains in large cap equities reflected the extraordinary performance of a handful of companies rather than broad participation across the market.

What to Watch

The upcoming earnings season will provide the first meaningful test of whether AI-related earnings growth can justify the extraordinary concentration that developed during Q2. With growth, value, and momentum portfolios all increasingly exposed to many of the same companies, even modest disappointments could affect multiple investment styles simultaneously.

Conversely, another quarter of strong earnings, continued AI infrastructure spending, and sustained investor enthusiasm could extend leadership further.

Whether market gains continue to depend on a handful of semiconductor companies, or begin to broaden across the technology sector, will be a defining question in Q3.

Theme 3: Market Breadth Improved Beneath the Surface

While large-cap leadership remained narrow, improving small-cap breadth suggested the conditions for broader market participation were beginning to emerge.

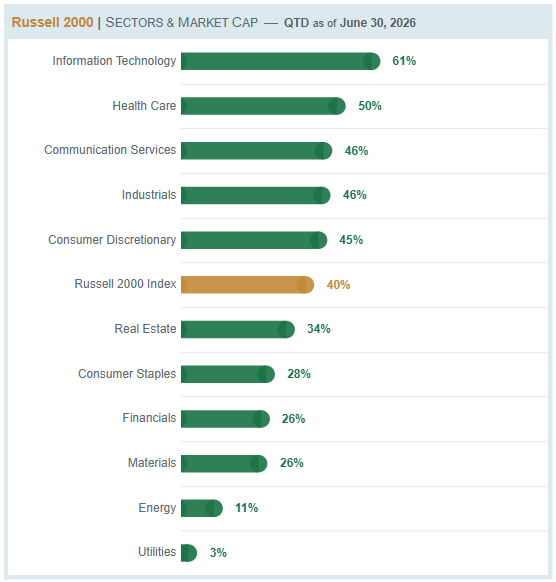

Figure 3:

Percentage of stocks within each sector that outperformed the Russell 2000 and S&P 500 indices – Q2 2026

The Russell 2000 Index was among the best-performing major U.S. indices, supported by much broader participation across sectors. Information technology, health care, and industrials all outperformed the Russell 2000 Index, while sector breadth consistently exceeded comparable levels in large cap equities.

Overall, 40% of Russell 2000 stocks outperformed their benchmark, compared with 30% in the S&P 500 and 31% in the MSCI World Indexes which indicated that market breadth improved beneath the surface despite continued concentration in large-cap equities.

Historically, sustained small-cap leadership has been more consistent with improving economic expectations than with late-cycle deterioration. Combined with stronger internal breadth, Q2 suggested investors increasingly anticipated lower interest rates, improving liquidity, and broader economic expansion beneath the headline concentration in large-cap technology.

What to Watch

The most important question for Q3 is whether improving breadth translates into realized market leadership. Continued outperformance from Industrials, Health Care, Financials, and small- and mid-cap equities would suggest the bull market is becoming healthier and less dependent on a handful of mega-cap technology companies. The relative performance of equal-weighted versus capitalization-weighted indices, together with sector and industry breadth, will provide some of the clearest evidence of whether market leadership is truly broadening.

Taken together, the three themes from Q2 suggest that the market enters the second half of 2026 on stronger footing than headline concentration alone would imply. The moderation of geopolitical risks has supported robust investor sentiment and improved the conditions for broader market participation. Whether those trends translate into broader market leadership will likely define the next stage of this bull market.

About Intech

Intech is a global quantitative asset manager that applies advanced mathematics and systematic portfolio rebalancing to harness a reliable source of excess returns and a key to risk control – stock price volatility. Intech applies its investment approach across five investment platforms which differ by risk-return objective: relative or absolute.

Intech also integrates fundamental-based information to identify stocks with favorable underlying characteristics, complementing its volatility-based models that target stocks with attractive trading profit potential due to their volatility characteristics.* These strategies only differ by the client’s desired benchmark and risk budget and include enhanced equity, active equity, defensive equity, extension equity, and absolute return investment solutions within the U.S., global, and non-U.S. regions.

*There can be no assurance that such models or characteristics will result in profitable investment outcomes, nor that any such positioning will achieve its intended results.