2025 Global Equity Review and 2026 Outlook

Executive Summary

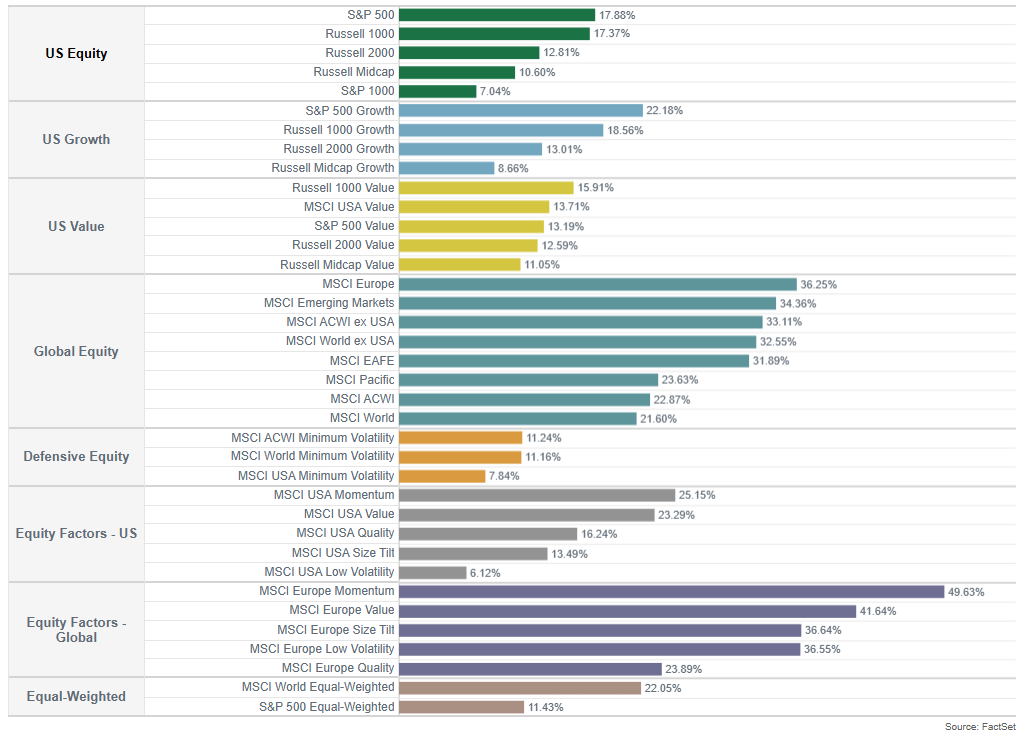

- Global equity markets posted robust gains in 2025, with the MSCI All Country World Index advancing 22.87% to record highs, marking one of the strongest years in recent memory.

- A significant rotation unfolded with international and emerging markets outperforming the U.S. by the widest margin since 2009.

- Non-U.S. equities (MSCI ACWI ex-USA Index) surged 33.11%, driven by strong earnings recovery, AI enthusiasm in Asia, and a weaker dollar.

- U.S. large-caps delivered solid but comparatively modest returns (17.88% for the S&P 500 Index), powered largely by mega-cap technology and AI-related capital investment, amid ongoing concerns over concentration and potential bubble risks.

These observations reflect broad market behavior and do not represent the performance of any Intech strategy or client portfolio.

Figure 1:

Strong Performance for Equity Markets in 2025

Past performance is not indicative of future results. Index performance is shown for illustrative purposes only. Indexes are unmanaged, are not available for direct investment, and do not reflect the deduction of management fees or other expenses.

U.S.-based artificial intelligence continued to dominate as a transformative force, fueling massive infrastructure spending, earnings momentum in select sectors, and periods of elevated volatility including sharp drawdowns from tariff announcements and competitive challenges such as China’s AI advances.

For active equity strategies, the environment created meaningful challenges as markets operated with selective leadership, elevated risk preference, and rising dispersion. Narrow stock gains were driven primarily by AI and technology mega-caps, while FOMO-driven buying on dips sustained elevated risk appetite. Dispersion widened substantially, with large spreads between stock winners and losers as well as between U.S. and international markets. These conditions tested portfolio construction, particularly for approaches that rely on broad participation and risk balance rather than concentrated exposure.

Looking forward to 2026, the backdrop remains constructive. As tariff-related policy headwinds moderate, labor markets cool without significant disruption, and AI-driven capital investment broadens beyond U.S. hyperscalers into global supply chains and infrastructure, opportunities may continue to evolve.

Diversification across geographies, sectors, and styles may help investors navigate a range of potential outcomes amid lingering risks such as high valuations, inflation stickiness, or shifts in AI productivity realization.

2025 in Review: Markets Adjust to a New Growth Regime

Global Performance and Market Structure

Equity markets in 2025 transitioned away from macro-driven returns toward a more fundamental and earnings-based environment. U.S. equities posted solid gains, but international developed and emerging markets delivered stronger performance as sector composition and earnings momentum favored non-U.S. regions.

Within the U.S., headline index returns masked important crosscurrents. Growth indexes outperformed value indexes as large technology-oriented companies continued to lead. At the same time, the underlying value factor outperformed the growth factor, indicating broader participation beneath index leadership.

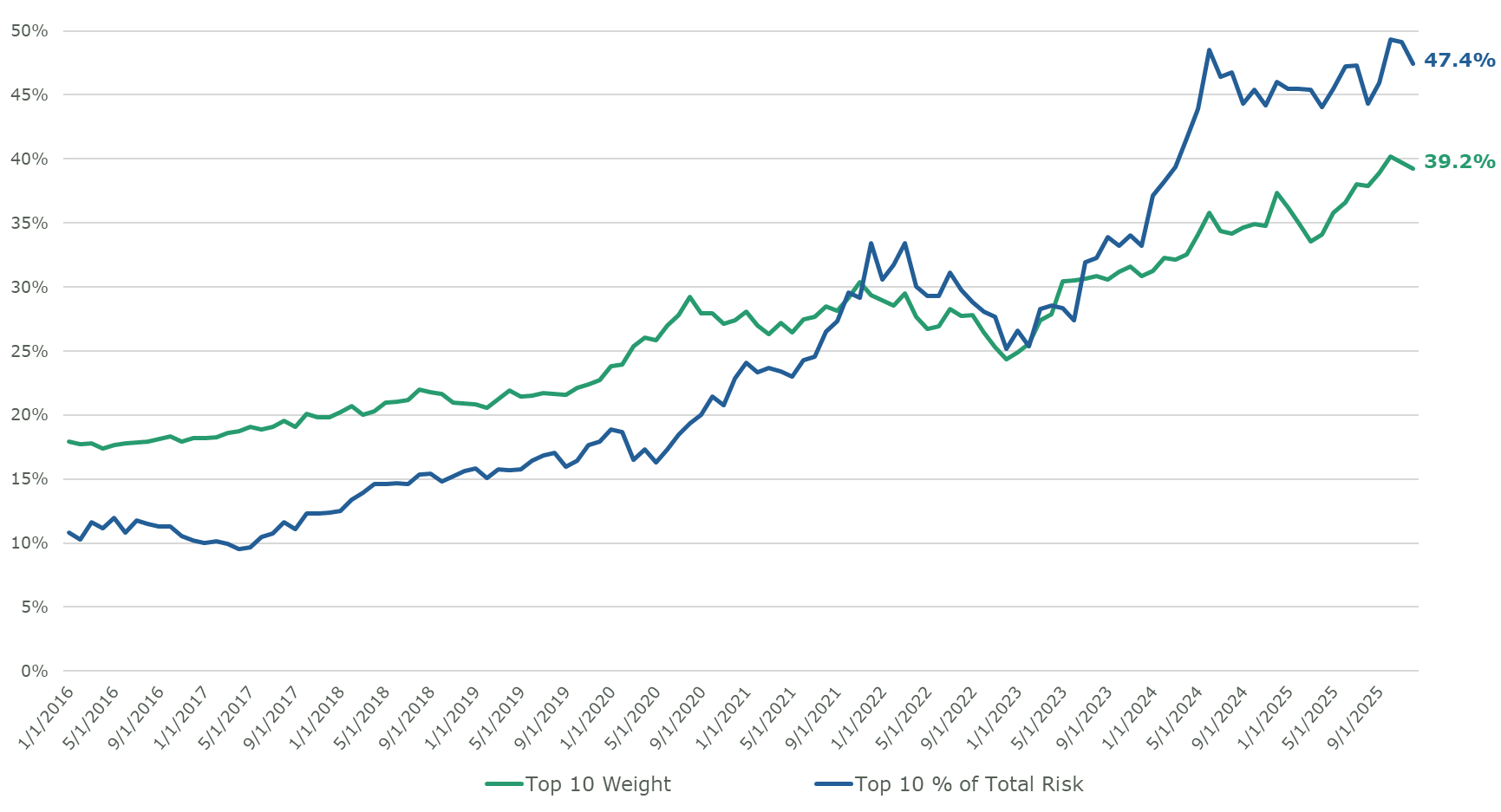

However, small- and mid-capitalization stocks lagged large-cap stocks as investor attention remained concentrated in the largest companies. The 10 largest U.S. companies represent 2% of the constituents in the S&P 500 Index and collectively account for nearly 40% of the index’s total market capitalization and explain about half of the total risk (See figure 2).

Defensive sectors and lower-beta strategies underperformed as investors favored higher-risk stocks, reinforcing a market environment dominated by selective leadership and rising stock-specific risk.

Figure 2:

A Few Names Dominate Risk in the U.S.:

S&P 500 Index Top 10 Stocks as % of Total Risk

10 years as of December 31, 2025

Source: FactSet. Indexes are unmanaged and not available for direct investment. Past performance is not indicative of future results.

Artificial Intelligence: Opportunity and Capital Intensity

Artificial intelligence remained central to market behavior. Investors broadened their focus beyond infrastructure leaders such as NVIDIA and Microsoft toward companies applying AI to improve productivity, efficiency, and profitability across industries including healthcare, logistics, manufacturing, and retail.

This transition amplified both opportunity and volatility. Surging capital expenditures for data centers, semiconductors, and energy infrastructure raised concerns about the sustainability of near-term returns, while demand increased for utilities, power equipment providers, and renewable energy firms. AI functioned not only as a growth theme but also as a catalyst for structural change in capital allocation.

Corporate Earnings Strength

Corporate earnings provided a critical foundation for equity market performance in 2025. Profit growth remained resilient across most major regions, supported by stable demand, improving operating leverage, and disciplined cost management. While margins faced pressure from elevated capital spending and wage costs in select sectors, productivity gains, pricing power, and continued revenue growth allowed many companies to exceed expectations. Earnings revisions trended upward through much of the year, reinforcing investor confidence and contributing to the durability of the equity advance.

Regional Developments

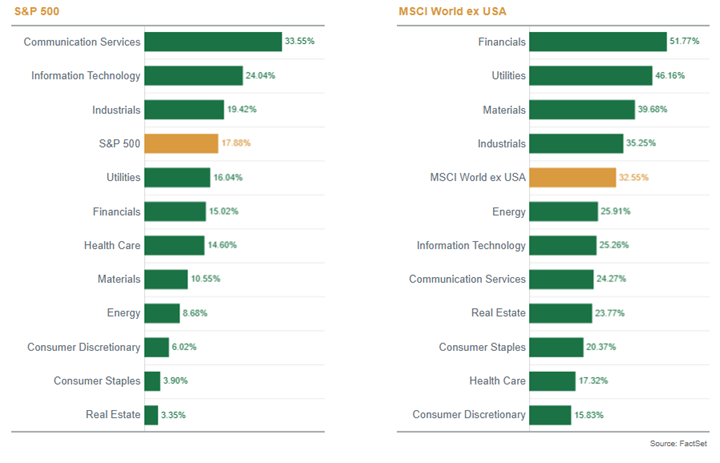

A significant rotation unfolded as international and emerging markets outperformed the U.S. by the largest differential since 2009. European equities advanced as financials, utilities, and industrials surged, although sector performance remained narrowly concentrated, with only three sectors outperforming in the MSCI World ex-USA Index

(see figure 3).

Japanese equities rose as corporate governance reforms strengthened and wage growth accelerated. Emerging markets delivered strong gains amid improving growth expectations and continued sector rotation. In this environment, the momentum and value factors ranked among the strongest drivers of international equity performance during the year.

Figure 3:

2025 Narrow Sector Performance

Source: FactSet. Past performance is no guarantee of future results. An index is unmanaged, is not available for direct investment, and does not reflect the deduction of management fees or other expenses.

2026 Outlook: From Shock Absorption to Forward Momentum

Economic Resilience and Policy Normalization

The U.S. economy enters 2026 with notable durability. Despite policy uncertainty, growth concerns, and trade frictions, the economy absorbed stress without significant damage to demand, employment, or investment. As constraints ease, several reinforcing dynamics support renewed forward growth momentum. The labor market continues to cool without freezing; rising unemployment reflects improving labor force participation rather than accelerating layoffs. Real wages remain positive, sustaining consumption while easing inflationary pressure.

At the same time, there was a moderation in policy headwinds. Policymakers have moved monetary policy closer to neutral, markets have stabilized financial conditions, and businesses have reduced their exposure to tariff and trade uncertainty. The upcoming appointment of a new U.S. Federal Reserve Chair in 2026 may further reinforce market stability by strengthening policy continuity and reducing uncertainty.

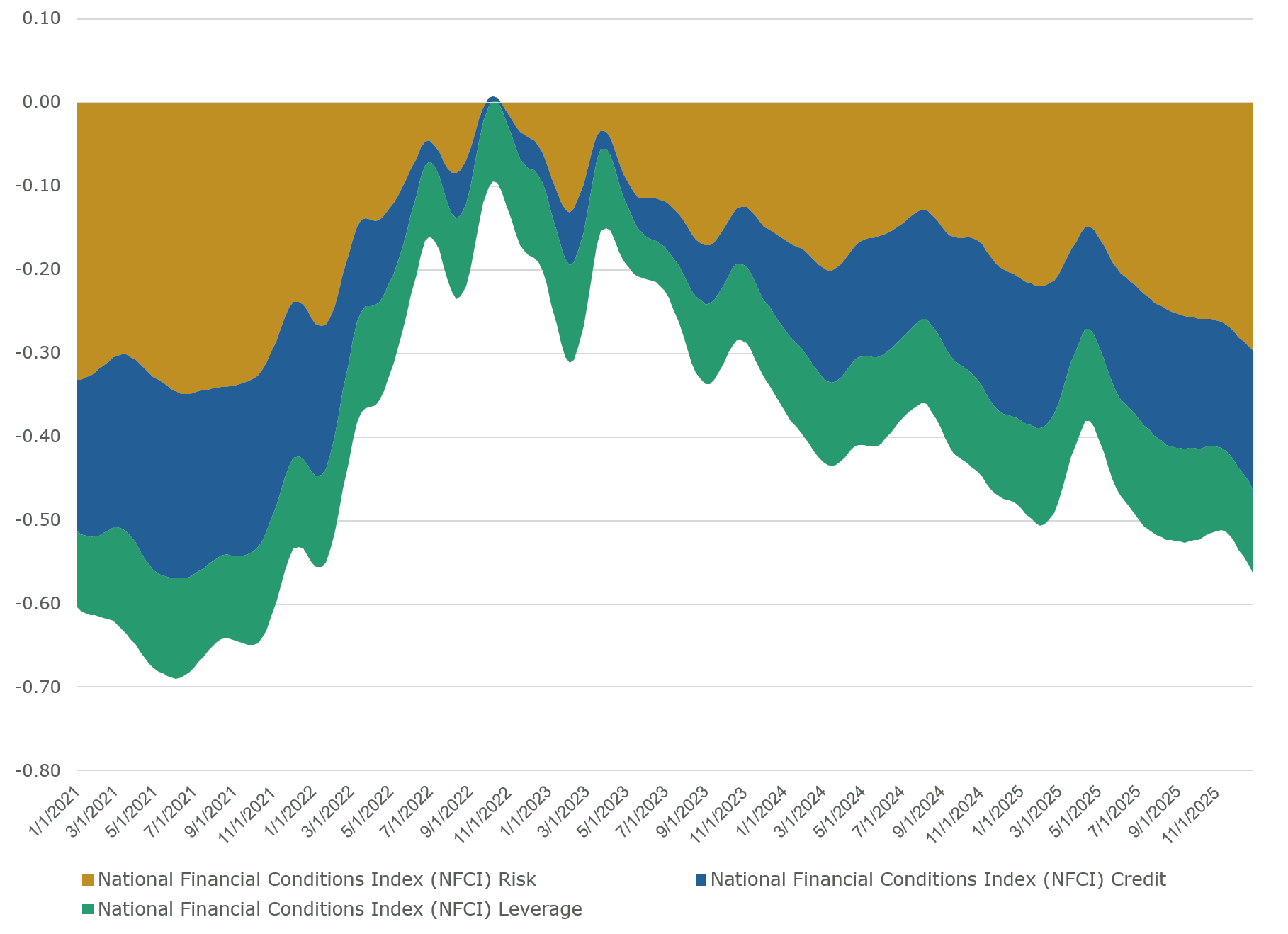

Meanwhile, the yield curve continues to normalize constructively, with lower short-term rates easing pressure on households, banks, and businesses while stable long-term yields reflect confidence in underlying growth, a configuration that historically supports equity markets. Collectively, these factors could support global growth and corporate earnings, although outcomes remain uncertain.

Figure 4:

National Financial Conditions Index (NFCI) Continues to Ease

Source: Federal Reserve Bank of Chicago. National Financial Conditions Index (NFCI). The National Financial Conditions Index (NFCI) is a composite index published by the Federal Reserve Bank of Chicago that measures risk, credit, and leverage conditions in U.S. financial markets. This material reflects market conditions at a point in time and is subject to change. The index is for informational purposes only and does not represent the performance of any investment. You cannot invest directly in an index.

Capital Formation and Inflation Dynamics

In the U.S., capital investment now extends beyond the domestic cycle. Non-residential fixed investment tied to artificial intelligence, semiconductors, energy, and manufacturing has become a key driver of growth, reinforced by rising foreign direct investment that anchors future construction, employment, and supply-chain development.

Regulatory and tax policy have become more supportive at the margin for U.S. corporations, as improved policy visibility and tax predictability enhance project viability and accelerate capital formation.

Inflation increasingly acts as a guardrail rather than a headwind. Productivity-enhancing investment, moderating wage pressure, and easing energy costs reduce the likelihood that stronger growth reignites inflation, allowing earnings growth and margin expansion to proceed with greater stability.

Market Structure, AI Adoption, and Sentiment

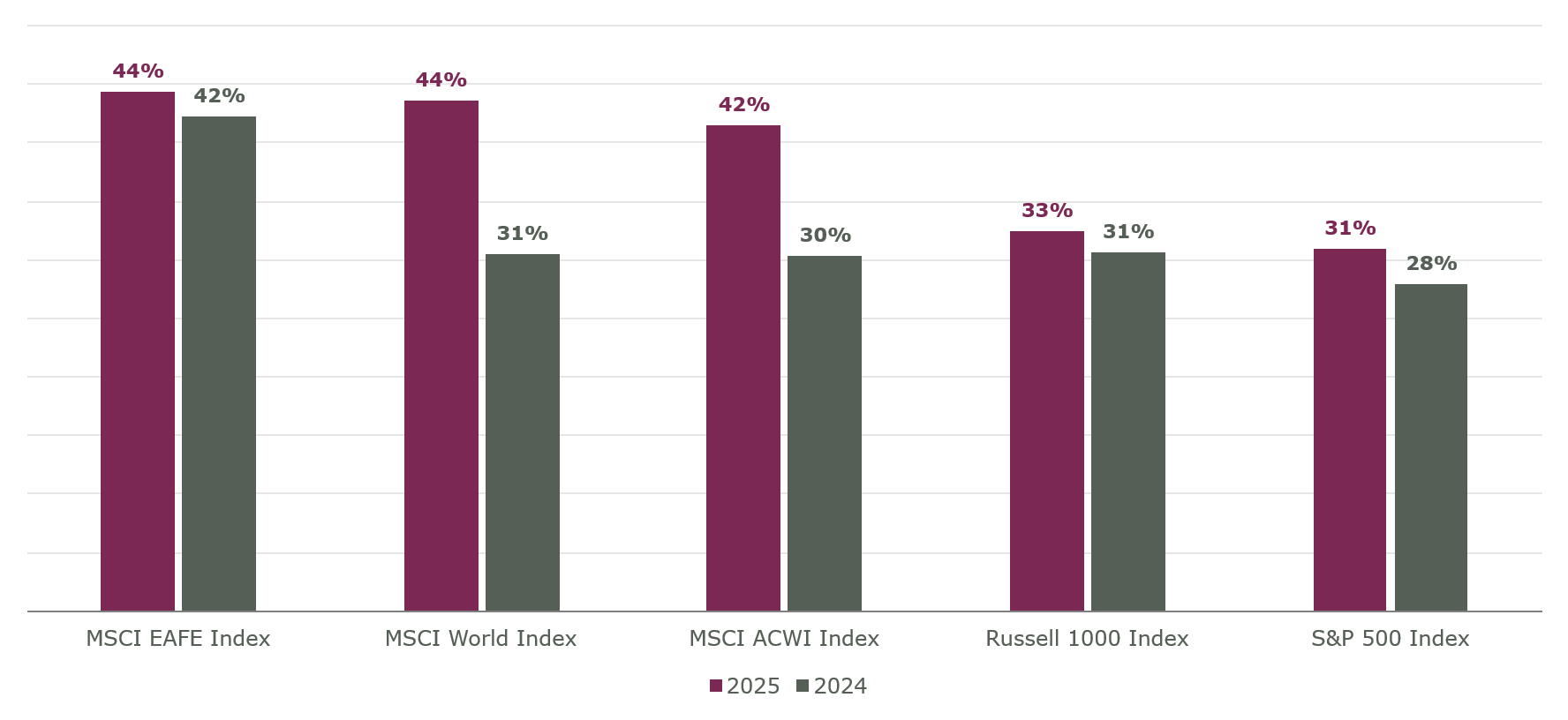

At the market level, global equity leadership continues to broaden as we observe a greater percentage of stocks outperforming in 2025 vs the prior year (see figure 5). The increase was noticeable in global universes, but we expect concentration to ease in the U.S. over time as non-mega-cap and non-technology sectors participate more meaningfully in returns, signaling a healthier market structure.

Figure 5:

2025 Equity Market Breadth: Percentage of Stocks Outperforming in Indexes

Source: FactSet. Past results are not indicative of future results. An index is unmanaged, is not available for direct investment, and does not reflect the deduction of management fees or other expenses.

Furthermore, AI optimism continues to shift from infrastructure toward adoption, with value creation increasingly favoring companies that use AI to improve margins, efficiency, and competitive positioning which supports broader earnings participation. Volatility increasingly reflects fundamentals as macro shocks recede, with company-level differences in execution, balance sheet strength, and earnings quality driving outcomes more directly.

Equity markets may also benefit from a reopening of IPO activity as financial conditions stabilize. High profile offerings can reinforce market confidence and broaden participation.[1]

Risks and Discipline

Our outlook remains conditional. Inflation could reaccelerate, rising data-center buildout may introduce incremental risk to bank loan portfolios, or labor market rebalancing could turn into contraction. Trade disruptions, earnings disappointment, or geopolitical shocks could increase volatility and trigger drawdowns.

Valuations also warrant potential caution. As of mid-December 2025, the Shiller CAPE ratio exceeded 40, a level historically associated with subdued long-term forward returns. While such valuations do not predict timing, they reduce the margin for error and reinforce the importance of diversification and selectivity.

Conclusion: Implications for Investors

For diversified strategies, the environment created meaningful challenges as markets operated with selective leadership (e.g., narrow gains driven by AI/technology mega-caps), elevated risk preference (e.g., FOMO buying dips), and rising dispersion (e.g., large spreads between stock winners/losers; U.S. vs international). These conditions tested portfolio construction, particularly for approaches that rely on broad participation and risk balance rather than concentrated exposure. We believe this market structure reinforces the importance of disciplined diversification and systematic rebalancing.

Looking ahead to 2026, the opportunity set appears increasingly favorable for active and systematic strategies. As economic growth stabilizes, policy uncertainty recedes, and market leadership broadens, we think dispersion and stock-specific risk should remain elevated, creating a fertile environment for capturing both fundamental and portfolio-level return opportunities.

In this setting, investors who emphasize flexibility, risk control, and rebalancing may be better prepared to navigate changing regimes and pursue durable long-term outcomes.

About Intech

Intech is a global quantitative asset manager that applies advanced mathematics and systematic portfolio rebalancing to harness a reliable source of excess returns and a key to risk control – stock price volatility. Intech applies its investment approach across five investment platforms which differ by risk-return objective: relative or absolute. Intech also integrates fundamental-based information to identify stocks with favorable underlying characteristics, complementing its volatility-based models that target stocks with attractive trading profit potential due to their volatility characteristics. These strategies only differ by the client’s desired benchmark and risk budget and include enhanced equity, active equity, defensive equity, extension equity, and absolute return investment solutions within the U.S., global, and non-U.S. regions.

-

These observations are illustrative of market sentiment only and do not reference any investment opportunity. ↑