A notable market development in 2026 is that we’re in the early stage of earnings diffusion. It does not yet represent a full regime shift, but I believe the direction is becoming increasingly clear.

Industrials and capital goods companies are now benefiting from sustained capital expenditure tied to AI infrastructure, reshoring initiatives, and defense spending. Utilities and energy-linked assets have also regained investor attention as growing data center demand increases electricity consumption and drives additional grid investment. Additionally, healthcare and select service sectors are showing early signs of productivity gains linked to AI adoption. Financials, especially those tied to capital markets, have stabilized as conditions improve.

Earnings revisions still favor mega-cap tech stocks, but leadership is no longer as narrowly concentrated as it was previously. In another early sign of broader market participation, SMID and small-cap stocks have also begun to outperform large caps at points this year.

This change matters. Markets tend to de-polarize when the opportunity set expands, not when leadership collapses.

The AI Trade Is Broadening

The AI theme itself has evolved in 2026.

The first phase of the cycle focused on builders, including semiconductors, hyperscalers, and infrastructure providers. That trade continues to work, but it no longer represents the only way to express AI exposure.

Recently, a second phase centered on productivity has started to emerge. Companies outside technology sectors have begun to integrate AI into workflows, improve efficiency, and incrementally expand margins. These changes are relatively new, but they signal an important transition.

Further, U.S. equity markets have started to move from a concentrated capex cycle toward a more distributed earnings cycle. If this trend continues, it could become a vital force for reducing market polarization.

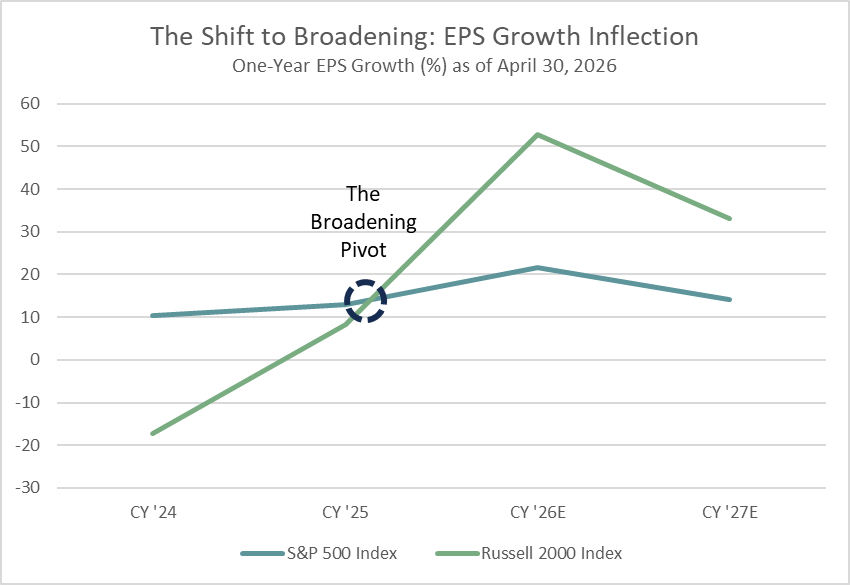

Figure 1:

The 2026 Inflection

Earnings growth for the Russell 2000 Index is projected to surpass the S&P 500 Index, signaling a potential structural end to market polarization.

Macro Conditions Have Become Less Restrictive

The macro backdrop has also shifted modestly in a more supportive direction (albeit not without new risks). Financial conditions have eased at the margin; however, geopolitical tensions have reintroduced volatility. Despite this, credit spreads have stabilized, rate volatility has declined, and confidence in a soft landing has improved.

These changes reduce the premium investors place on mega-cap balance sheet strength. They also allow more intermittent and rate-sensitive parts of the market to participate more meaningfully. For example, small caps and cyclicals have already shown episodic, but inconsistent, outperformance.

I believe these factors may indicate that macro has not fully turned, but it no longer reinforces concentration as strongly as it once did.

Positioning Has Started to Normalize

Positioning has also begun to evolve. Mega-cap AI trades remain crowded, but incremental flows have become less concentrated. Investors have started to revisit under-owned segments including small caps, value stocks, and emerging markets.

Rotations, when they occur, now extend more broadly across sectors. This shift suggests that the marginal buyer has become more diversified. Investors have not fully repositioned, but they have begun to reallocate capital at the margin. That is often how market regimes change.

What Has Not Changed Yet

Despite these developments, market polarization has not fully broken.

Mega-cap technology stocks still lead earnings growth. The market has not yet tested the durability of AI monetization. Although SMID and small-cap indices have outperformed large caps on a year-to-date basis, that outperformance has been uneven and not yet decisive.

These conditions may suggest that the process has started, but it has not yet been completed.

The Most Likely Path Forward

The market is unlikely to experience a sharp break in polarization. Gradual normalization appears more likely.

That process would involve AI expectations stabilizing as investors shift focus from capex to returns. Earnings growth would continue to broaden, particularly as productivity gains spread across sectors. Macro conditions would remain supportive enough to allow wider participation. Leadership would rotate incrementally rather than abruptly.

This path differs from a scenario where mega-cap technology stocks decline sharply. Instead, it implies a multi-quarter transition driven by improving fundamentals elsewhere.

The Signal That Matters

Investors should focus less on price action and more on earnings breadth.

If a larger share of companies deliver positive earnings revisions, if margins expand outside the technology sector, and if revenue growth becomes less concentrated, then polarization will unwind in a structural way. Until then, rotations will likely remain partial and episodic.

Conclusion

Equity markets have spent the past two years in a state of extreme concentration. In 2026, early signs of change have started to appear, driven not by weakness in the leaders, but by gradual improvement across the rest of the market.

That distinction is critical. Polarization does not end when the dominant trade breaks. It ends when it no longer needs to carry the entire market.

About Intech

Intech is a global quantitative asset manager that applies advanced mathematics and systematic portfolio rebalancing to harness a reliable source of excess returns and a key to risk control – stock price volatility. Intech applies its investment approach across five investment platforms which differ by risk-return objective: relative or absolute.

Intech also integrates fundamental-based information to identify stocks with favorable underlying characteristics, complementing its volatility-based models that target stocks with attractive trading profit potential due to their volatility characteristics.* These strategies only differ by the client’s desired benchmark and risk budget and include enhanced equity, active equity, defensive equity, extension equity, and absolute return investment solutions within the U.S., global, and non-U.S. regions.

*There can be no assurance that such models or characteristics will result in profitable investment outcomes, nor can there be assurance that any such positioning will achieve its intended results.