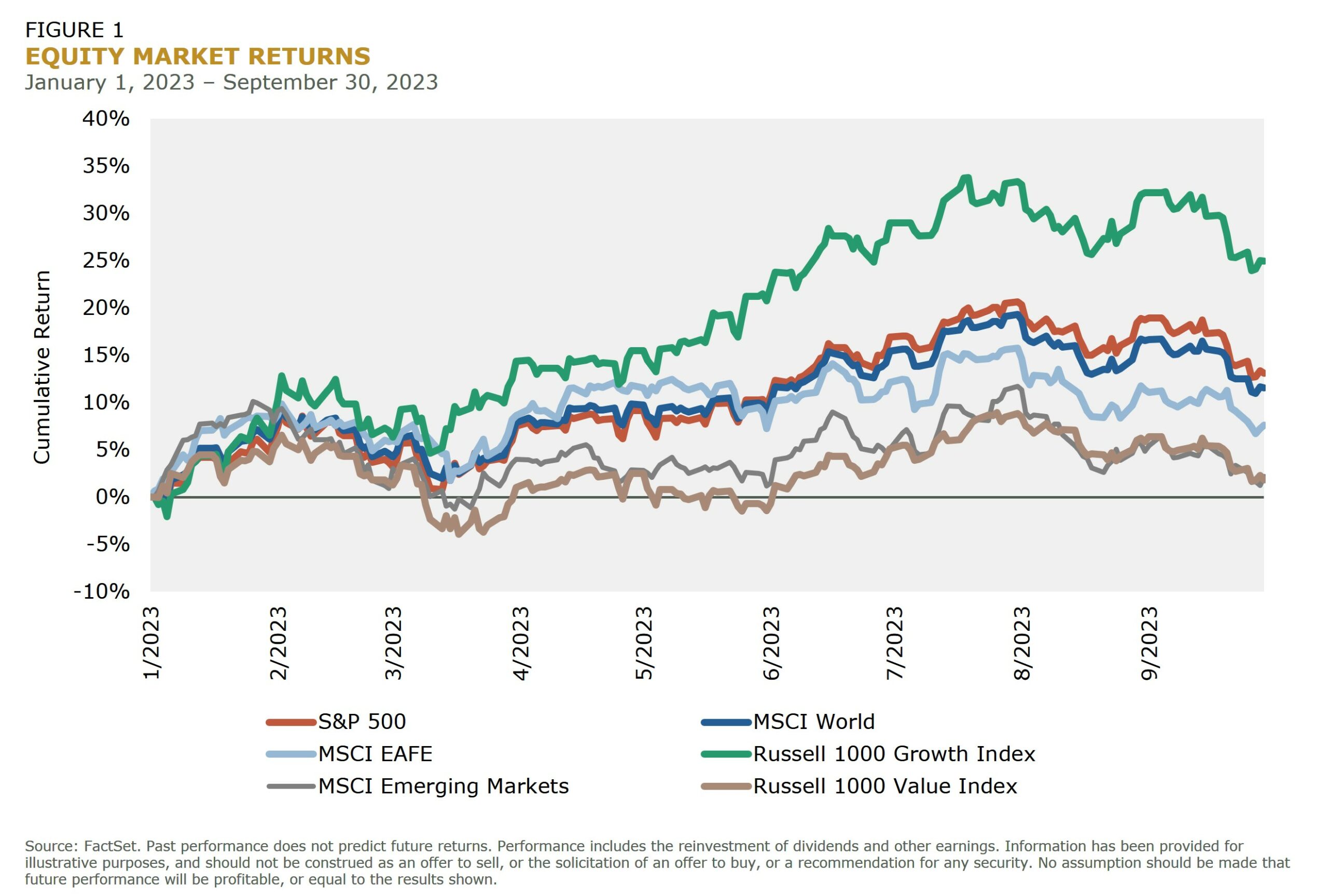

After a bullish start to the year, equity markets turned back from recent highs in the third quarter. The prospect of lingering inflation and “higher for longer” interest rates weighed on valuations for risk assets like equities, despite corporate earnings outperforming most estimates. Broader global markets are still significantly outpaced by U.S. large cap growth stocks on the year, though their outsized influence on returns did take a breather in the last few months.

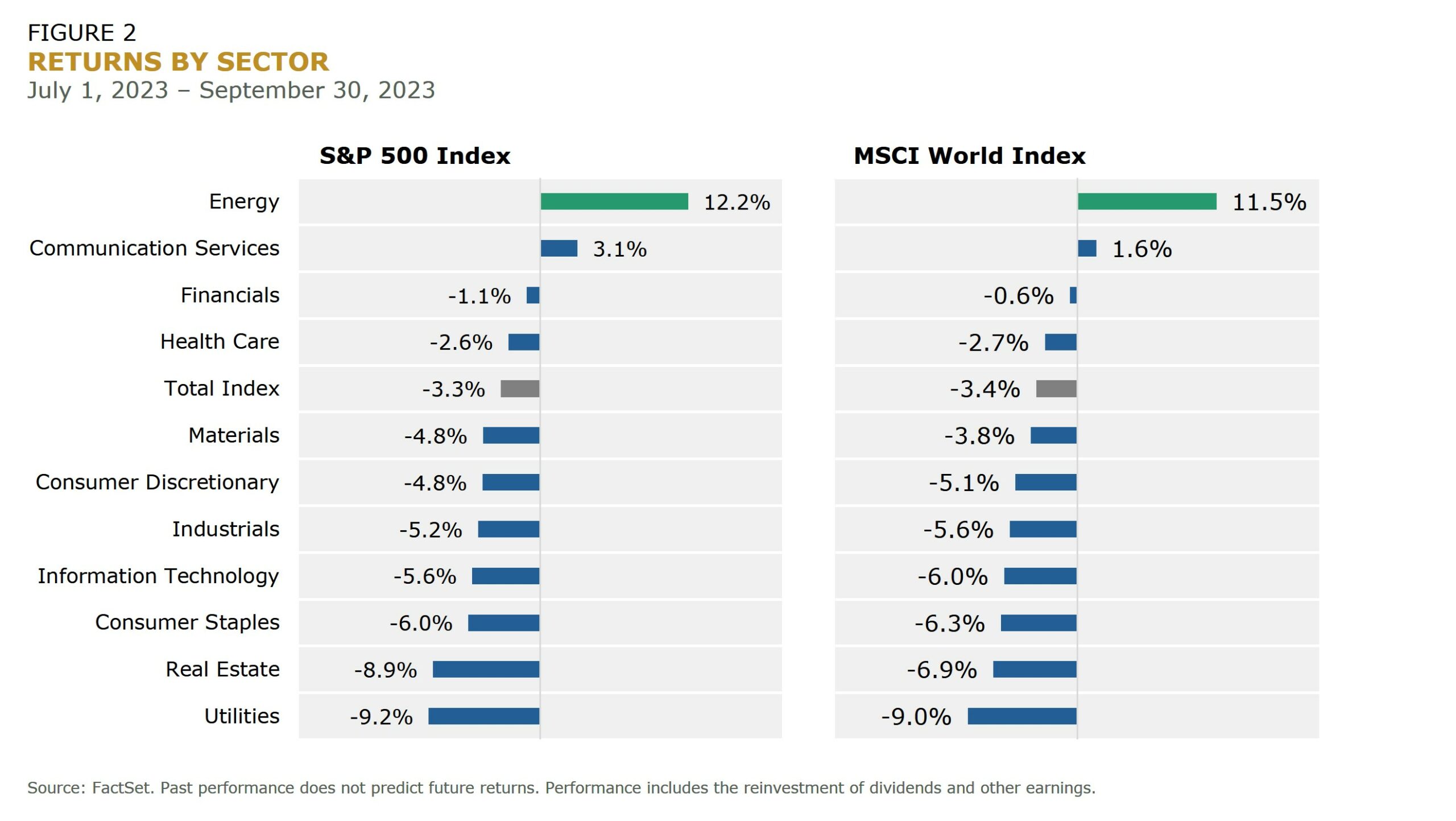

Energy Lead, Defensive Sectors Lagged

The sell-off in the equity markets during this period was widespread, impacting 9 of 11 GICS sectors. Only communication services and energy outperformed, with the latter buoyed by a surge in oil prices on the way to outperforming the total S&P 500 by more than 15%. Rising interest rates were also a headwind to defensive sectors such as utilities and consumer staples stocks, which are typically impacted by rising yields in fixed income securities.

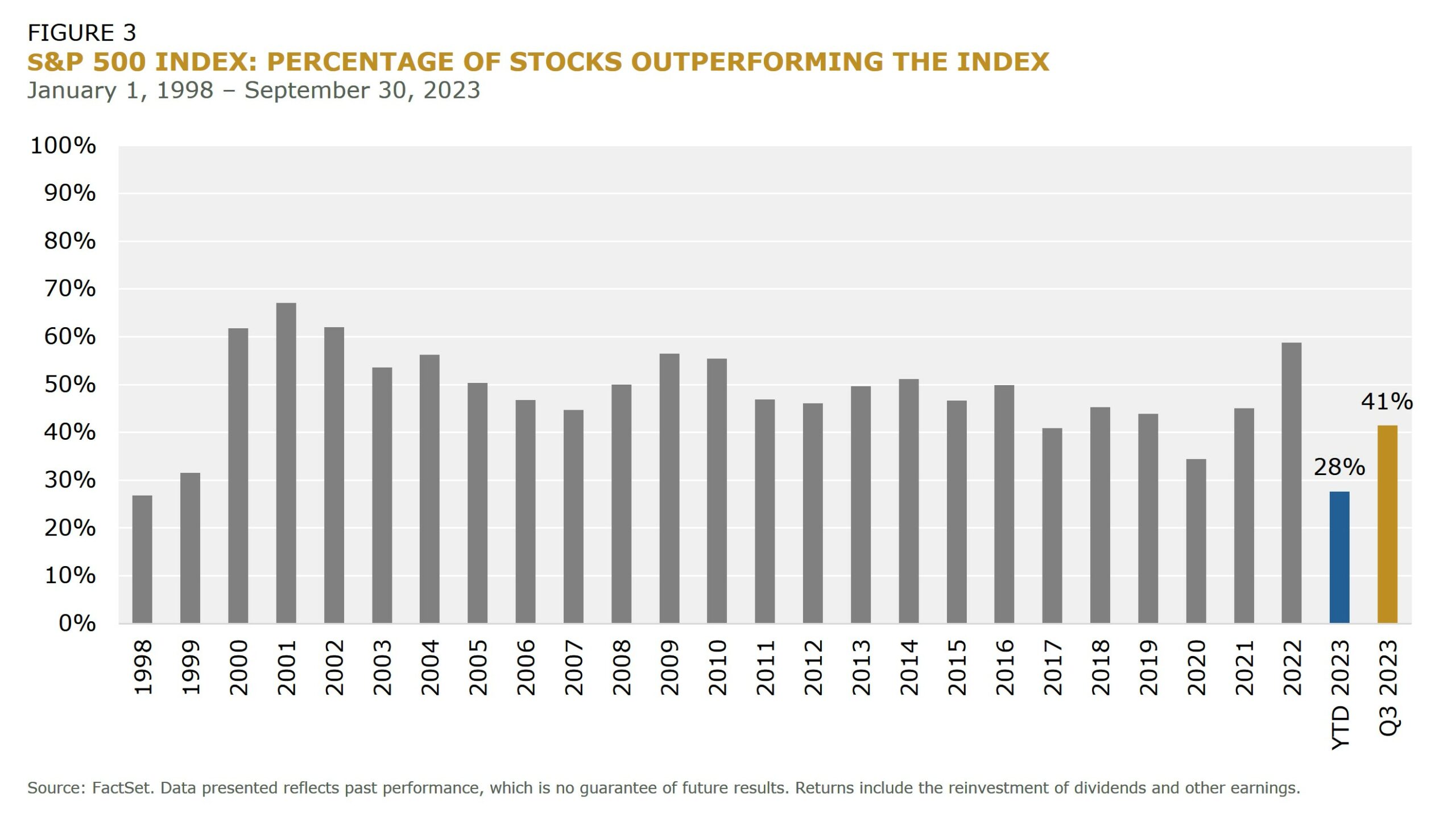

Market Participation Broadened

As we alluded to earlier, U.S. large cap growth stocks have dramatically outperformed other markets this year, leading to narrow leadership. One interesting indicator of broader market participation is the percentage of stocks outperforming the index. Year-to-date, only 28% of S&P 500 stocks outperformed the total index, a level not seen since the late 90s. However, this number increased to 41% in the third quarter, moving closer to the historical norm of a more even distribution of winners and losers.

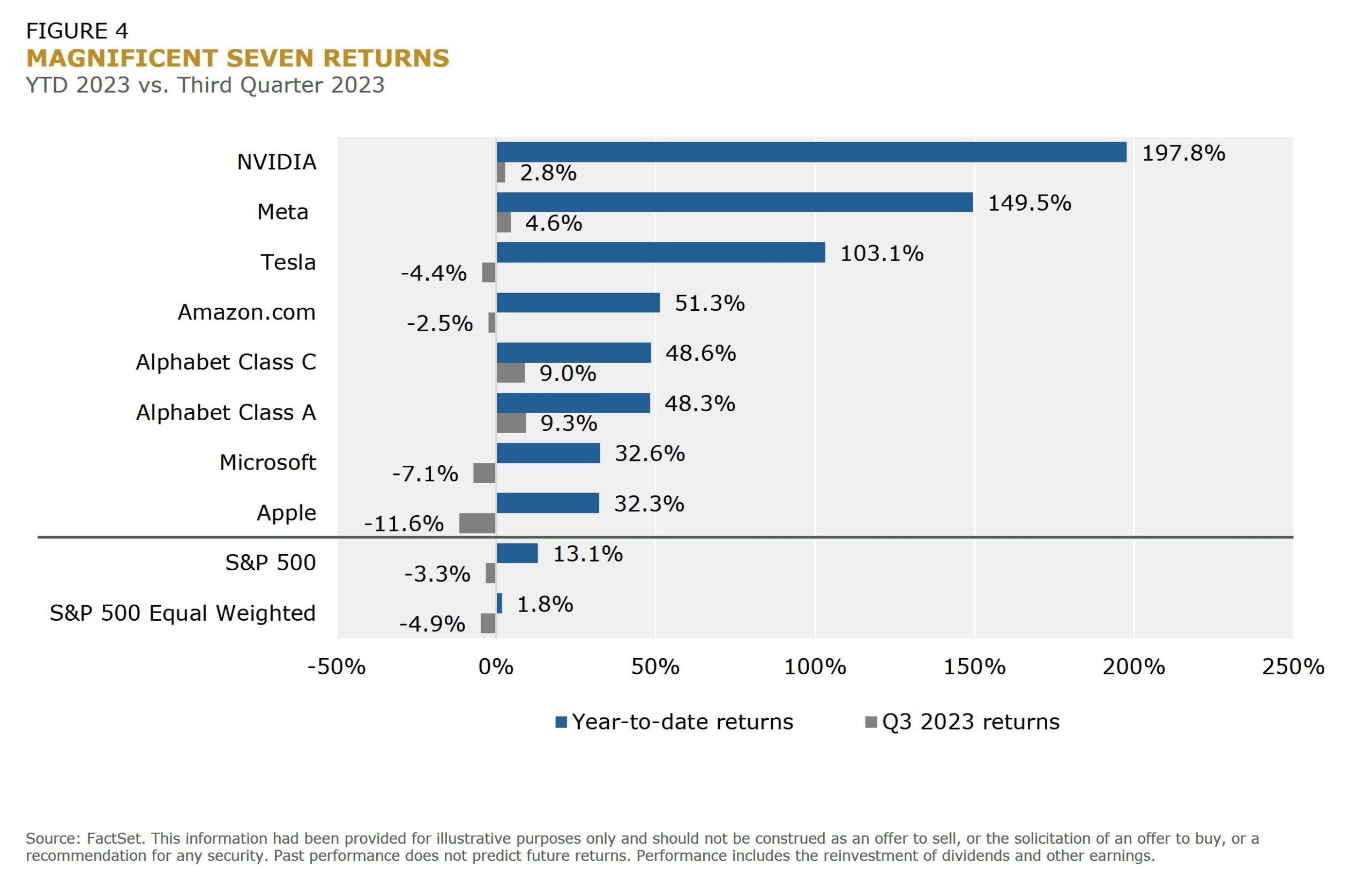

Mixed Results from Mega Caps

The dominance of mega-cap tech stocks, often referred to as the ‘Magnificent Seven,’ in driving equity market returns has been a focal point in recent quarters. These heavyweights played a significant role in fueling bullish U.S. equity returns in the first half of the year. However, as indicated in last quarter’s blog, the narrow leadership of the market has come and gone before, and this past quarter showed a return to more balanced and diverse market dynamics – at least for now.

Uncertain Economic Outlook

Economists and market pundits continue to present a wide range of potential outcomes for the next 12-18 months. This spectrum includes the possibility of a painful recession or a “soft landing.” The post-pandemic economy has been a challenge for the U.S. Federal Reserve to navigate, with conflicting data making it difficult to discern the direction of developed economies.

While some positive indicators, such as a resilient labor market, suggest a relatively sunny outlook for the U.S. in the near term, ongoing issues like government dysfunction and persistent inflation, coupled with emerging geopolitical risks, have not inspired much confidence among market participants.

Stocks and Bonds: A Correlation Renewed

One development that is challenging the diversification strategies within traditional asset allocation strategies is the renewed correlation between stocks and bonds. Anxiety related to interest rates has triggered sell-offs in both asset classes, often leaving investors with nowhere to hide. If this relationship continues, it may challenge the traditional role of treasuries as a ballast against equity volatility. Other hedging solutions, such as options, can also come at a cost, acting as a material drag on long-term returns if they don’t pay off frequently enough.

Despite these challenges, the fact is that substantial equity exposure remains a necessity for most institutions. The key is to navigate these turbulent waters with innovative, active strategies designed to weather the forces within the markets and the exogenous macroeconomic shocks that influence them.

The Path Forward

This quarter brought about a shift in the equity markets relative to the first half of 2023, impacting sector performances and challenging the dominance of mega-cap tech stocks. The economic outlook remains uncertain, with a wide range of potential outcomes, and the correlation between stocks and bonds poses new challenges. In this environment, innovative, active strategies will be crucial in charting a course through the unpredictable landscape.